UK Electric Vehicle and Battery Production Potential to 2040 – update published June 2022

Growing optimism for the UK battery manufacturing industry but redoubling of efforts needed to keep pace with investments across Europe.

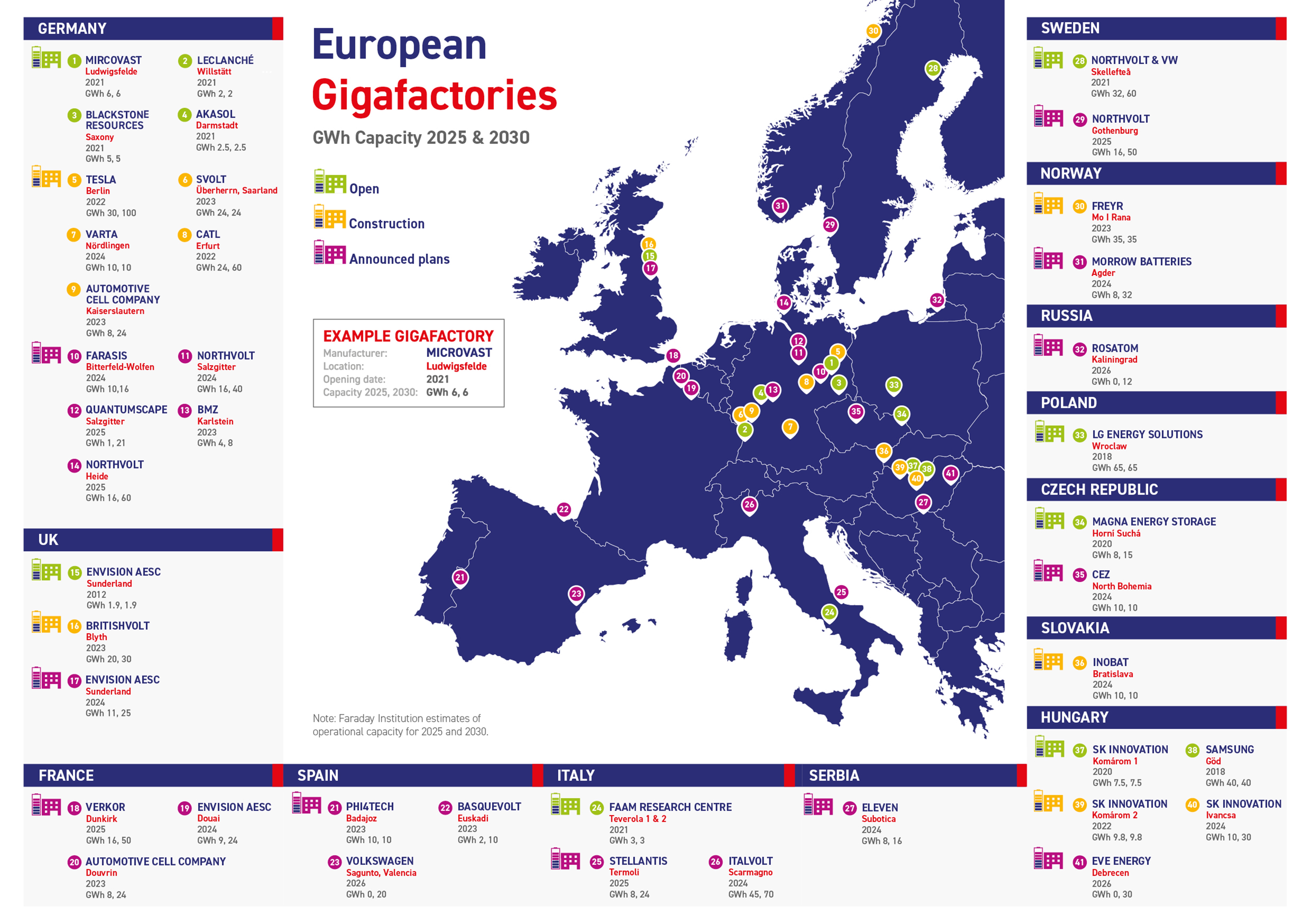

The Faraday Institution predicts that there will be demand for ten UK-based gigafactories (large, high volume battery manufacturing facilities) by 2040, each producing 20 GWh per year of batteries.

The transition to electrified transport is essential to meet Net Zero commitments. The size of the economic opportunity provided by this change is significant. Recent announcements in the UK by Britishvolt and Envision AESC have built excitement, particularly in the North East, about the potential to create a new, dynamic and highly skilled battery industry in the UK.

The UK Government has played its part by making bold policy commitments and increasing investor confidence in the UK as a location to do business.

But more needs to be done.

The UK is making progress but not moving fast enough compared to its European competitors. UK battery manufacturing plants could reach a combined capacity of 57 GWh by 2030, equivalent to around 5% of total European GWh capacity, compared with 34% in Germany.

It is important that UK Government continues to communicate the attractiveness of the UK as a battery manufacturing location to investors. Alongside cultivating new investors, it should also help to develop a resilient, sustainable and efficient supply chain, build up skills capability and commit to the long-term funding of battery research, particularly next generation batteries.

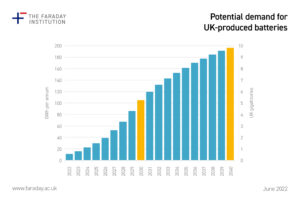

The UK needs to move quickly to secure investment in new gigafactories. By 2030, around 100 GWh of supply will be needed in the UK to satisfy the depend for batteries for private cars, commercial vehicles, heavy goods vehicles, buses, micromobility and grid storage. This demand is equivalent to five gigafactories, with each plant running at a capacity of 20 GWh per annum. By 2040, demand rises to nearly 200 GWh and the equivalent of ten gigafactories.

The UK needs to move quickly to secure investment in new gigafactories. By 2030, around 100 GWh of supply will be needed in the UK to satisfy the depend for batteries for private cars, commercial vehicles, heavy goods vehicles, buses, micromobility and grid storage. This demand is equivalent to five gigafactories, with each plant running at a capacity of 20 GWh per annum. By 2040, demand rises to nearly 200 GWh and the equivalent of ten gigafactories.

Download the report, “UK Electric Vehicle and Battery Production Potential to 2040.“

Continued efforts needed

The UK Government, industry stakeholders and research organisations should celebrate the recent successes but keep up the pace and focus. The shake-up and unprecedented change in the global automotive industry will create winners and losers. The UK needs to grab the opportunity with concerted and coordinated effort by:

- Continuing to communicate the attractiveness of the UK as a global and regional battery manufacturing location to global investors;

- Identifying prospective sites for gigafactories and the construction of associated physical, transport and energy infrastructure by the local, regional and national government;

- Developing the requisite electric vehicle (EV) battery skills and training infrastructure;

- Providing long term commitment to mission-based research into next generation batteries that are cheaper, lighter weight, longer-lasting, safer, manufacturable and fully recyclable;

- Developing a strategy to localise and create an efficient, resilient and sustainable UK supply chain to improve availability and affordability of key battery materials for battery production; and

- Developing a strategy to create the conditions for a new lithium-ion battery recycling industry in the UK to flourish.

Summary of changes in key outputs of the report from 2020 update.